Managing pocket money or a stipend is the first step to financial freedom for students. Handling a limited monthly allowance well is not just about cutting back—it’s about building sensible habits, making better choices, and learning early how money works. Here’s a comprehensive, practical blueprint for young adults to take charge of their finances and avoid common pitfalls.

Why Money Management Matters for Students

-

Avoids debt traps and financial stress.

-

Builds a foundation for wealth, goal achievement, and peace of mind.

-

Prepares for emergencies and retirement by developing saving and investing habits.

-

Boosts confidence and independence in financial decisions.

Step-by-Step Guide to Managing Pocket Money or Stipend

1. Build a Realistic Budget

-

List all income sources: allowance, stipend, part-time jobs, scholarships.

-

Categorize expenses: essentials (food, rent), education (books, stationery), transportation, health, and personal or fun spending.

-

Include both regular (food, phone plan) and occasional expenses (gifts, events).

-

Set clear limits for each category, revisiting your budget monthly to adjust as needed.

2. Track Every Rupee Spent

-

Use budget apps or a notebook to note every expense. Even small daily spends add up.

-

Regularly review spending to spot patterns—where do you overspend? What can you cut?

-

Keep receipts or note digital transactions for accountability and clarity.

3. Prioritize Needs Over Wants

-

Cover basic needs first—accommodation, groceries, bills, and essential study materials.

-

Delay non-essential purchases (gadgets, outings, impulse shopping); use the “24-hour rule” to curb impulse buys.

-

Avoid “spending for social approval”—choose personal priorities over peer pressure.

4. Make Savings Automatic

-

Set up a recurring deposit or automatic transfer to a savings account—aim for at least 10% of monthly income, even if it’s just ₹100–₹500 to start.

-

Treat your savings as mandatory, not optional—it’s “pay yourself first.”

-

Separate savings for special goals: travel, gadgets, or big events.

5. Create and Protect an Emergency Fund

-

Set aside a small amount each month (e.g., ₹500–₹1,000) until you have at least ₹5,000–₹20,000 saved.

-

Use this fund only for real emergencies—never for routine spending.

-

Keep this fund separate from everyday accounts to prevent accidental use.

6. Cut Unnecessary Subscriptions & Recurring Fees

-

Review streaming, magazine, club, and app subscriptions regularly—cancel what you don’t use.

-

Choose prepaid or student plans that fit your real needs and budget.

7. Make the Most of Student Discounts and Offers

-

Always carry a student ID for offline and online deals (travel, shopping, food, electronics).

-

Combine discounts with cashback or coupon apps for double savings.

-

Only buy what’s truly needed—avoid shopping just for the sake of a discount.

8. Practice Smart Buying: Bulk & Online Shopping

-

Shop for books/stationery in bulk to save with student offers or at wholesale outlets.

-

Use e-commerce sites for better rates, especially on essentials and tech, but avoid spending just to score a deal.

9. Earn Extra Income Where Possible

-

Pick up part-time jobs, internships, or freelance gigs for pocket money and valuable work experience.

-

Use the income to balance immediate needs and build savings.

10. Borrow and Lend Responsibly

-

Borrow from friends only if truly necessary—always repay promptly and record every transaction.

-

Avoid lending money you can’t comfortably do without and never enable overspending in others.

11. Manage Borrowing and Credit Carefully

-

Use debit over credit to control spending.

-

Avoid taking loans or credit cards unless essential, and always know repayment terms.

-

Never use credit for daily expenses or fun; it’s a tool for building credit, not for lifestyle upgrades.

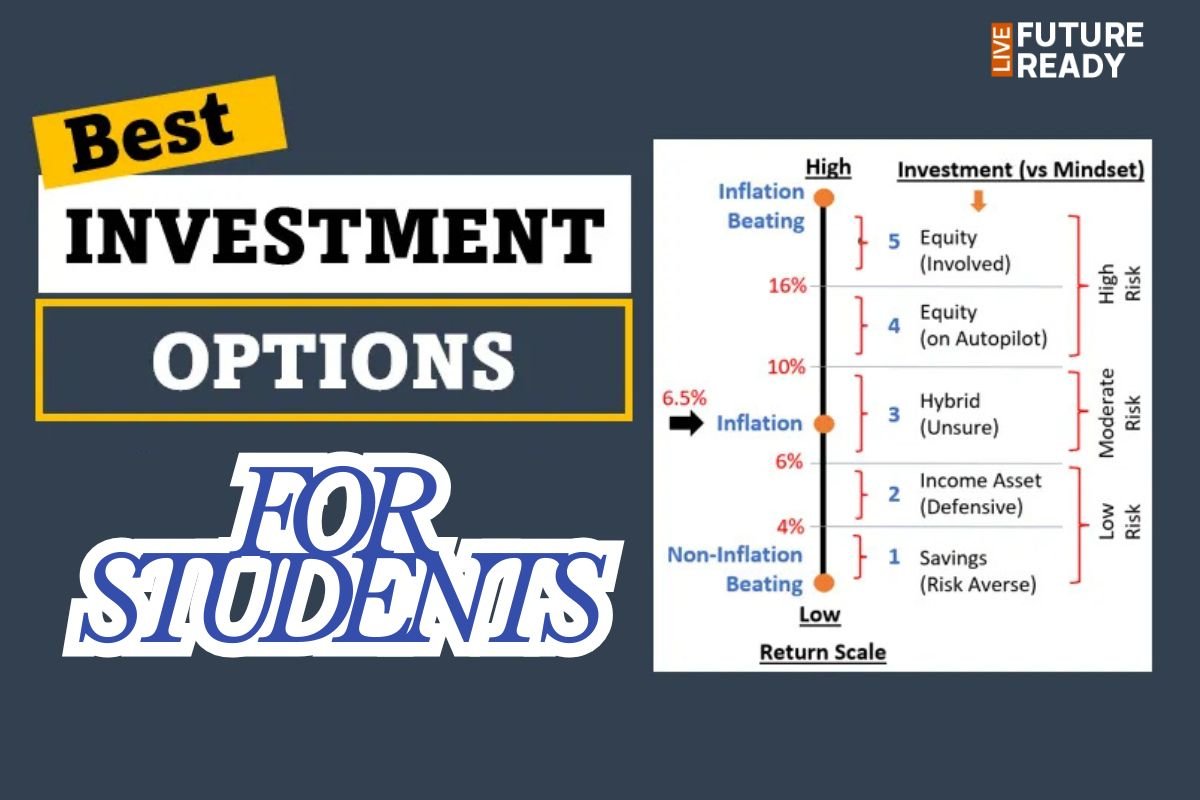

12. Invest Early—Even Small Amounts

-

Research simple, low-risk investment options: recurring deposits, SIPs, or mutual funds suited for students.

-

Use free financial literacy resources (blogs, apps, workshops) to build knowledge and decide where to invest.

13. Regularly Review and Adjust

-

Set aside time monthly to revisit your budget, check savings targets, and reflect on money habits.

-

Adjust your plan for income changes, new responsibilities, or goals.

14. Upgrade Your Financial Skills

-

Stay informed by reading finance blogs, following personal finance influencers, or attending workshops.

-

Use educational finance apps to learn and practice skills: digital wallets, micro-investments, or budgeting tools.

15. Stay Mindful of Student Loans

-

Take student loans only as a last resort; know the terms and commit to timely repayment.

-

Explore scholarships, financial aid, or part-time work as alternatives to borrowing.

Common Student Money Mistakes to Avoid

-

Overspending on wants and status symbols.

-

Ignoring the importance of budgeting and tracking.

-

Using credit or loans for lifestyle expenses.

-

Failing to save or start an emergency fund.

-

Blindly copying friends’ spending habits.

Final Thoughts

Managing pocket money or a stipend is about more than counting coins—it’s about shaping a healthy financial future. By budgeting, tracking, saving, making smart purchases, and learning continually, students set themselves up for financial strength and freedom in adulthood.